After a tough start to the week all round, global markets appear to be rallying. The US stock market rose sharply yesterday, October 16, after technology stocks had plummeted last week losing millions for investors and shaking global markets.

The Dow Jones reported its best day since March 2018 after Morgan Stanley reported third-quarter earnings higher than predicted, alongside Dow members Goldman Sachs, Johnson & Johnson, and United Health.

The Dow was up over 500 points, the S&P gained 2.1% and the Nasdaq 2.9%.

Netflix beat all expectations and its shares soared more than 14 percent in after-hours trading. Morgan Stanley’s better than expected results were driven by a 15 percent rise in investment banking revenue.

Global Markets – Shanghai Shows Slight Rise

On opening today, China’s markets had also rallied somewhat after a prolonged sell-off. The benchmark Shanghai Composite Index rose just over 1%.

China’s stock markets have been struggling with internal economic issues and the ongoing trade war with the US. Last week China’s markets hit their lowest point in four years.

Cryptocurrency Market Capitalization

Cryptocurrency markets also plummeted last week, mirroring the US stock markets and dropping billions from the overall market capitalization for all cryptocurrencies.

After a sudden upturn and fall back on October 15, the market has leveled somewhat. Bitcoin’s price is again hovering around the $6,500 mark.

Gold Prices

Gold, often a go-to in times of uncertainty, saw a two-month high on October 15. Lukman Otunuga, Research Analyst for FXTM commented to CNBC:

“While the sell-off in stocks rekindled some demand, there were other key factors in play. With escalating trade tensions, concerns over slowing global growth, geopolitical tensions and U.S. mid-term election jitters in the mix, gold has a chance to shine.”

Otunuga’s comments support predictions by investment firm Incrementum found in their chartbook summary titled In Gold We Trust.

Experts and analysts aren’t celebrating too much just yet, though, as the threat of a potential recession as well as trade and political turmoil is fuelling what might be a rocky road for all markets for some time yet.

At the time of writing, and the opening of the US markets, the Dow has fallen 200 points so far today amidst the ongoing volatility.

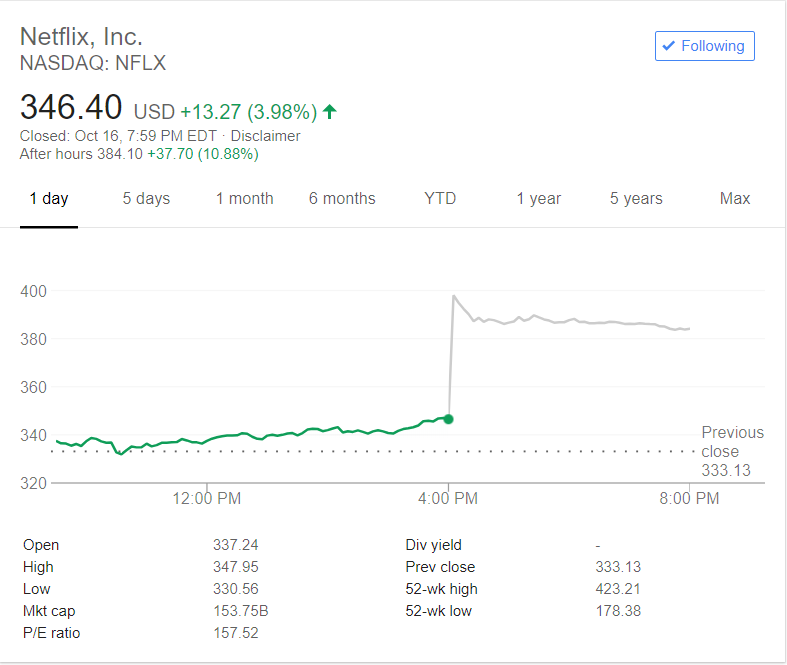

Whoever said that Tuesday was going to be a rough one for Netlifx investors (no finger pointing here), ended the day with mud in their eye as Netflix stock (NASDAQ: NFLX) soared by a massive 15% (trading at 11% up after the bell rang) after the company announced its third-quarter earnings report.

Netflix Smashes Its Q3 Records

After missing its quarter two targets by 1 million subscribers stock went into a tailspin, leaving investors blindsided. But it looks as if the online streaming service provider has been working hard since then, smashing its target of 5 million new subscribers and racking up an impressive 6.96 million. 1.09 million of these are US-based with a further onboarding of 5.87 million overseas.

Netflix Stock Wednesday

Earnings per share (EPS) was adjusted to 89 cents versus the 68 cents estimated and revenue was impressive as well, at $4 billion. Although international revenue declines by some $90 million due to YOY impact from currency, this figure was still higher than it was during Q3 of 2017.

As per the Sensor Tower estimates, it looks like Netflix is back to the high-speed growth that Wall Street had become accustomed to, having increased revenue by 36% in Q3. CEO Reed Hastings said after the report:

“We’re getting a little better on the forecasting.”

The Outlook for Netflix

Tuesday’s rally is certainly good news for the live streaming company and its investors but that doesn’t put it in the clear. There’s still the matter of the Goldman Sachs Monday warning about the price increase of producing content and competing against new players in the field. Moreover, Netflix will need to continue wooing new subscribers from abroad.

Break-neck speed is hard to maintain before someone ends up tumbling over. Whether or not Netflix stock will bound back and stay high remains to be seen, although yesterday’s shareholder party could get cut short at any time.

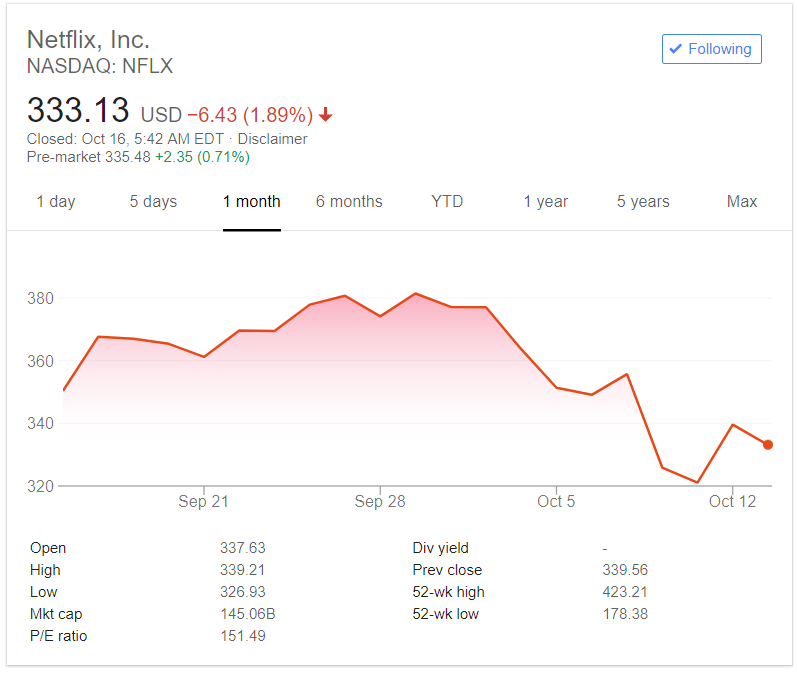

Tuesday is likely to be a difficult day for Netflix investors as they brace themselves for the Q3 earnings report. What was once (albeit briefly) the world’s most valuable media company and purveyor of binge-worthy series seems to be on an inevitable downward trend.

The media giant’s Q2 earnings report left shareholders shaken and stirred as Netflix’s forecasts were off by 1 million subscribers, a discrepancy the company blamed on its own internal forecasting.

Netflix Could Do No Wrong–Until It Started Doing Wrong

The subscriber stagnation revealed in July ran through Netflix stock like an aftershock and ended one of this year’s longest and strongest rallies. Netflix investors had previously seen shares double between January and mid-July. But the recent tech selloffs left and right have done nothing to boost investor confidence and Netflix stock could be set to take another hit.

By Monday of this week, its stock was trading at over 15% less than its $400 level of some months ago, during which time Netflix market cap had overtaken that of Walt Disney. However, despite the unexpected cold shower last quarter, Netflix bulls remain confident the stock will rally.

App analytics provider Sensor Tower pointed to the signs of increased growth that the market has grown accustomed to, with Q3 earnings from in-app subscriptions rising by over 90% YOY thanks to some 50 million new installations.

On top of that, Netflix is experiencing major growth in emerging markets like India and Brazil. And even US growth supposedly remains strong, despite fears of a stagnating market.

Q3 is also thought to have seen more people flock back to the platform thanks to new seasons of its most popular shows. American Vandal, Orange Is the New Black, and Sacred Games are all among subscribers’ favorites.

But the Long-Term Outlook for Netflix Investors Is Not so Bullish

Despite signals from Sensor Tower, Goldman Sachs issued a warning yesterday. Analysts say that even if Netflix does reach its targeted 5 million new subscribers for Q3, Netflix investors can still expect more conservative growth moving forward. Producing world-class content isn’t cheap and Netflix is likely to see a cash burn increase from $2 billion last year to 3.3 billion this year.

Goldman Sachs cut the price target from $470 to $430, pointing to Netflix competitors trading lower price-to-earnings ratios. Netflix is still trading at around 150 times earnings, much higher than the sector as a whole, and Goldman Sachs analysts stated that Wall Street:

“continues to underestimate the size of Netflix’s global addressable market, the impact of incremental content spending, and the growing value of Netflix to both distributors and content creators.”

Netflix is under constant pressure to keep hold of its subscribers and attract new ones by producing quality content and its content budget is estimated to reach an eye-watering $13 billion this year. As more and more rivals enter the video streaming market, including Apple, Disney, and even Snapchat, the pressure will only mount.

Facebook (FB.NASDAQ) was a great idea. So was MySpace for that matter. Apparently, people love to catalog their lives online, and Facebook has given them the perfect platform to do just that. Mark Zuckerberg’s dorm room project made him one of the richest people in the world. But the juggernaut that has been Facebook stock may be on the edge of collapse.

For everything that Facebook is, it isn’t a vital technology. They don’t produce anything tangible and rely heavily on advertising revenue to power their burgeoning infrastructure. Herein lies one of their biggest problems. In order to continue to demand big payouts from advertisers, Facebook has to maintain a loyal stable of global users.

Facebook Is Losing Face

The last year has been rough for Facebook’s public image. Cambridge Analytica was a wake-up call for anyone who understands how powerful social media can be in the political sphere, and a recent data breach cost 29 million Facebook users extensive amounts of highly sensitive personal information.

Let’s call all that Facebook’s ‘real’ problem. Betrayal, manipulation and being careless with important information isn’t going to win anyone any friends. But for Facebook, their issues only start with a questionable business model.

The other problem that could seriously affect Facebook from a financial point of view is their slowing revenue growth, potentially overvalued equity, and increasing reliance on niche platforms to drive growth. Right now FB is trading at around 23 times earnings, which has led many to speculate that it’s the buy of the century.

Picking up shares in other major tech companies could cost you a lot more. Twitter is trading at almost 100 times earnings, and Amazon stock is hovering just below 140 times earning at the time of writing. With other high-growth tech names trading at such high valuations, why is Facebook selling at such relatively low levels?

A Scary Scenario

The narrative that’s banging around the financial markets is that while FB isn’t the incredible growth story it once was, it’s still worth buying on a long-term basis. Numerous articles have been run over the last few weeks suggesting that FB makes sense to buy at current levels. But this is a seriously dangerous position.

Changes in the tech world are fast, and FB has entered a period of slowing revenue growth. Some estimates suggest that over the next few years Instagram will drive revenue higher, while FB’s core earnings stagnate. That may be the case, however, FB is facing bigger problems.

When more than 29 million Facebook users recently lost their data to hackers, the level of data collection that Facebook engages in was a surprise to many. Mark Zuckerberg has built up a data collection platform that would have been a wet dream for the East German secret police. For more than a decade, people from all over the world fell over each other to offer up their most personal data.

Today people are waking up to the reality that Mark Zuckerberg isn’t some cool young guy who wants to connect people. Instead, he is sucking up any information he can get his hands on, and selling it to the highest bidder.

People have only had a few months to digest the fact that their location, communications, and basically anything else Facebook can get in its servers is being stored for future use.

The realization of Facebook’s business model by the public could be a big negative for a company that relies on user trust to generate revenue.

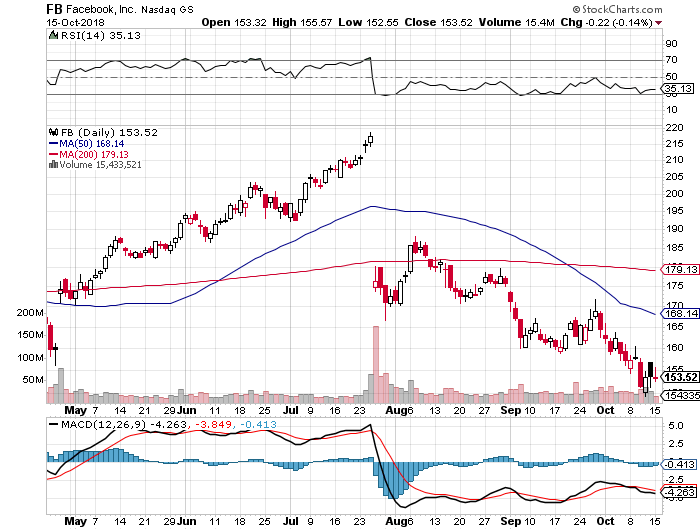

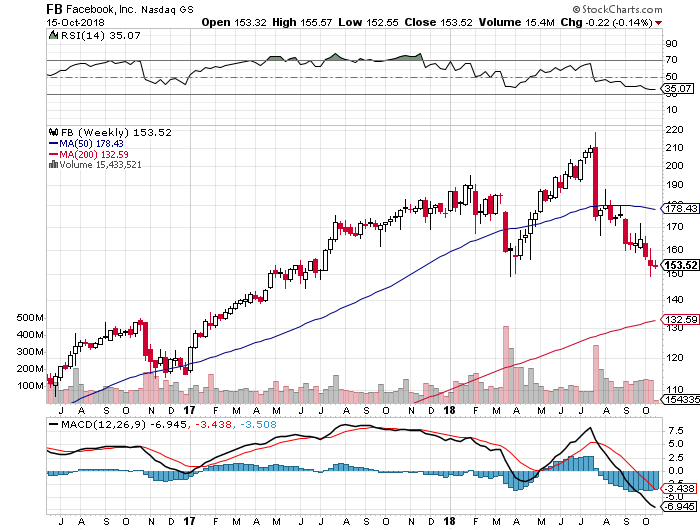

The Technicals Look Tempting, Like the Sirens of Circe

Facebook stock had an interesting summer. Their Q2 revenue miss caused a major sell-off (probably bot-driven), and then the stock seemed to snap higher. Now it has fallen back to the lows that it saw in March, and it is probably going to drop like a brick from here.

Facebook Daily Chart

The charts actually make FB stock look like a buy, which could sucker people into a major spanking. Both the daily and weekly RSI and MACD indicators are at oversold levels, which could mean that FB is on the edge of a major collapse.

Facebook monthly chart

Pay attention to that massive gap lower in July, and look at the volume that drove FB lower. That kind of selling is normal during a top, which is probably in for Facebook shares.

Stay Away From Zuk’s Mess

The existential crisis described above is just one of many problems that Facebook has to deal with. The tech company is also facing a massive fine within the EU and this dynamic could also punish a company that could be operating in violation of a multitude of foreign laws.

To what degree Facebook will be able to muddle through all of these issues is anyone’s guess. The company may fold, or see its operations severely curtailed over the next few years. From an investment standpoint, FB shares should be considered off-limits and could make a good short position for risk lovers.

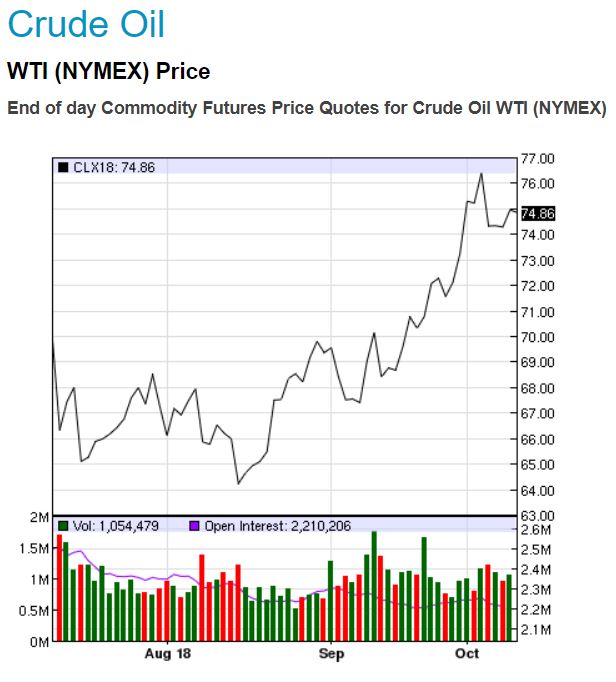

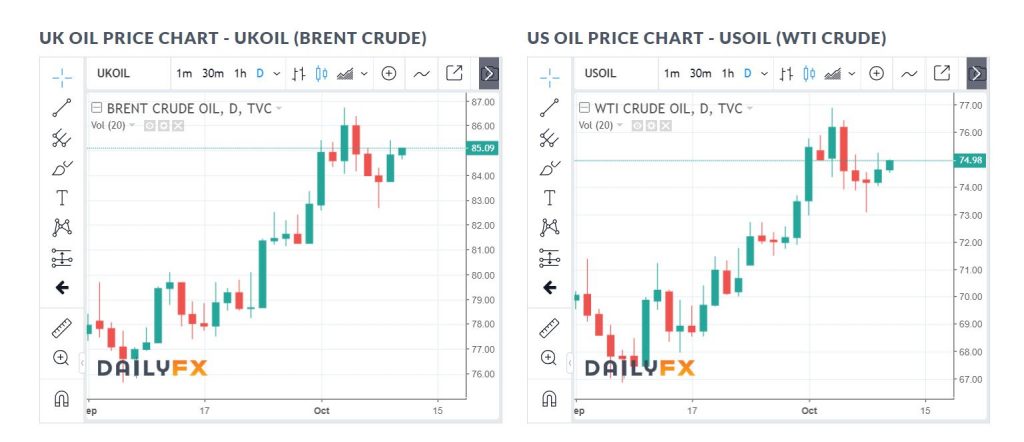

The price of oil is going through a veritable roller coaster ride. In July, there was a strong setback. The international oil cartel, the OPEC, decided to gradually increase production. Russia also turned on the valve. On top of that, some unscheduled delivery failures that existed in Libya had to be repaired.

But the correction seems to be over for the time being. Only the North Sea brand Brent climbed very quickly in the direction of $80 a barrel. And now there are new events. Now it is the US sanctions against Iran that are increasingly attracting investors.

The country, which incidentally is also a member of OPEC, will not be allowed to export any more oil from November of this year. And that could have serious consequences for the price of oil, at least that’s the fear of many investors.

What has been happening since mid-August in the oil market you don’t get to see so often. The price of Brent, which is relevant in Europe, has risen by 20%, to $84.6 a barrel. Since the beginning of the year, there has been 27% growth, since the middle of last year over 85%.

Certainly, given the fact that the price had plummeted in the previous years from $115 (mid-2014) to under $30 (January 2016), the current backlash is partly also a correction.

On the one hand, there is the booming economy, which boosts oil consumption and thus drives up the price.

And here comes the second reason into play. Traders fear a further decline in supply. This is limited only by the fact that oil production is falling in Venezuela due to the economic crisis.

Now the situation around Iran, the third largest producing state within the OPEC oil cartel, is also getting worse. The US imposed new sanctions on the Mullah regime. These will not come into effect until the beginning of November, but they cast their shadows. Russian Minister of Energy Alexander Novak said:

“The market is very nervous and very emotional.”

The fast price dynamics are not even pleasing production countries, let alone the consumers. This can be seen from various statements. For instance, US President Donald Trump has repeatedly complained that the OPEC needs to take responsibility for regulating the price. That is only partially true.

The cartel in alliance with Russia and some other oil states at the end of 2016 agreed on funding cuts. Due to the new market situation at the beginning of this summer, however, the taps turned up again.

The two largest producers Russia and Saudi Arabia said they were ready to do more if needed. But at least, as far as Russia is concerned, there are doubts as to whether it can further increase its historic maximum funding.

And so the price forecasts of $100 a barrel are increasing in the face of this mishap situation. According to Novak, the price range of $65 to $75 a barrel appears to be at a suitable level for both producers and consumers. We can already see that price is following his predictions.

Gasoline, Heating Oil and Gas Getting More Expensive

The average price of gasoline worldwide is $1.18 per liter. Due to the higher oil price, the consequent increase in fuel prices is already being observed. Although it’s still a bit early to think of the dark season, in terms of electricity and gas price, we can already feel it in the air.

Price increases indicate the turn of the year. Both heating oil and gas are becoming more expensive than last year in many regions. We must prepare to live in the new era of high prices.

Not the start to the week that traders were hoping for. After Friday’s brief rally, Asian stocks took another tumble on Monday with indexes in all major countries, including Hong Kong, Taiwan, and Australia off by more than 1% triggered by financial and tech selloffs. Japan’s Nikkei also fell more than 1% following one of its worst weeks of the year.

Financial Sector Hit Hard

After upbeat Q3 earnings reports from US banks like JPMorgan and Citibank, financial stock was among the worst hit this Monday morning across Asia. Mitsubishi UFJ saw a decline of 1.98%, and Mizuho Financial was also down by 1.60%

Japan’s Softbank down by more than 5%

Japan’s Softbank stock was hit hardest and down more than 5% this Monday. Fears of the bank’s close investment ties to the Saudi government surrounding global outrage over a journalist’s disappearance are thought to have triggered the plunge.

Hong Kong Suffering Tech Selloffs

Hong Kong stocks also took a drop following Friday’s bounce, with the Hang Seng HSI, off by about 1%, with tech selloffs leading the downward spiral. Among the biggest losers, there was social media giant Tencent, dipping by 2.5%, and AAC Tech, a smartphone component maker, falling by more than 4%.

In China, the markets were mixed. The Shanghai Composite was down 0.3% but the Shenzhen Composite was up 0.4%. Tech stocks also weighed heavily on Taiwan’s Taiex, pulling it down by 1.44%, and South Korea’s Kospi down 0.3%, led by tech heavyweights like Samsung taking a hit.

Australian Markets Also Down

Australian stock markets also saw a similar spiral down by over 1% with the financial sector leading the trend. The Commonwealth Bank of Australia, Australia and New Zealand Banking Group ANZ, and Westpac Banking were all down over 1% at the time of writing. Last week was New Zealand’s worst in eight and a half years according to Market Watch.

After an unexpected bearish start to the week’s trading in Asia, the question now is how will Europe and Wall Street open this Monday morning?

Yields of Italian Bonds Climb to Multi-Year Highs – Stocks Are Under Pressure

Matteo Salvini is not known for his restraint. On Monday, the Italian Deputy Prime Minister called for a verbal sweep of European Union Commission President Jean-Claude Juncker and Economic Commissioner Pierre Moscovici.

“The enemies of Europe are those sealed in the bunker of Brussels.”

These were his words at a press conference that Salvini held together with the head of the French right-wing populist, Marine Le Pen. The governing coalition in Rome, populist five-star movement and right-wing, is currently in the midst of Brussels’ budget policy for 2019.

The EU complains that the structural deficit, which excludes one-time effects and cyclical fluctuations, is increasing by 0.8% of annual economic output. However, the Commission has called for a 0.6% reduction in this deficit.

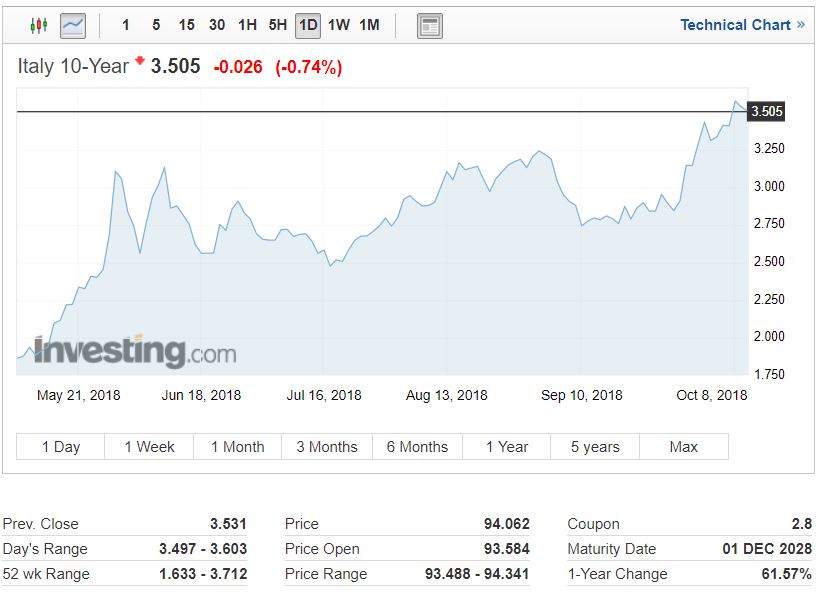

Italy 10-Year Bond Yield Overview

It is this disagreement that immediately led to negative effects on the financial markets last Monday. Yields on 10-year Italian bonds climbed to a four-and-a-half-year high.

“We are a bit surprised by the strength of the reaction in bond markets, but it appears the market is jumping to the conclusion that the European Commission will take a hard-line stance when Italy submits its budget.”

Said Antoine Bouvet of the investment bank Mizuho.

Higher refinancing costs can also hit Italian banks hard. According to calculations, the core capital of the institutions has already declined in the second quarter.

Italian banks traditionally hold the promissory notes of their country. If the prices of the securities fall, this will affect the capital calculations of the banks. On the stock market, the prices of some institutions declined. This also weighed on the lead index: It’s about to fall into a bear market.

Italy Stock Market (FTSE MIB)

Authorities Monitor Liquidity of Italian Banks

Given the turbulence of the past few days on the financial markets, there was a more intense observation of the Italian banks, it was reported on Tuesday. The audits cover both customer deposits and the interbank market. There is no reason to be alarmed.

European Banking Supervisors Taking Banks’ Liquidity Under Scrutiny

The budget dispute between Italy and the European Commission pushed the yield on the Italian 10-year bond to 3.72%, the highest level since February 2014. Italian banks are vulnerable here as they hold €375 billion of domestic bonds worth about ten% of their assets.

Depreciation on the value of bonds could tie up much of the banks’ equity, which is then no longer available for loans. According to CNBC, one of the Italian crisis banks, Banca Carige, met representatives of the European Central Bank on Wednesday.

The government in Rome wants to increase new debt in the coming year to 2.4% of the gross domestic product. This is three times as much as planned by the previous government.

The EU Commission has raised concerns and investors are also worried. Italy’s European Affairs Minister Paolo Savona said that if the pressure of the markets becomes too strong, there may be changes to the draft budget.

Chart of Italy Stock Market (FTSE MIB) Chart of Italy 10-Year Bond Yield Overview

After one of the worst weeks of the year for traders and tech billionaires alike, signs of a possible recovery were already showing last Friday. But, what’s in store for the week ahead? With several important developments on the horizon, here’s a market roundup of what you need to know before heading into next week.

Market Roundup for the Coming Week

Italian Budget Deficit

The deadline for EU countries to submit their draft budgets to the European Commission for the coming year is Monday, October 15. All eyes will be on Italy as the Mediterranean country is expected to present a plan for a 1.7% GDP structural deficit for the next three years. This won’t go down well with the Commission and could put significant pressure on the euro.

Brexit

Ever since the British public was given a voice, politicians and individuals alike wished they’d shut back up. Brexit negotiations so far have been like watching a slow-motion train crash with UK Prime Minister Theresa May leaping from one cringeworthy catastrophy to another.

Next week is a big one on the Brexit timeline with investors nervously viewing a trembling pound on Tuesday as the EU’s chief Brexit negotiator heads to Luxembourg for the latest round of damning criticism.

If this date sounds familiar, it’s because October 16 was the original deadline to sign off on the UK’s exit deal.

But since there is no deal so far agreed, that timeline had been kicked down the road for later this year. However, the UK pound is likely to react to Tuesday’s outcome, even if the talks are not definitive.

US Federal Reserve

After a largely unpopular move to hike interest rates that saw the stock markets around the world take a tumble, the minutes of the Fed’s meeting last month are available on Wednesday.

In spite of widespread criticism most notably from President Donald Trump, the emphasis will likely be on the plan to raise rates gradually over the coming year as opposed to the “out of control” rises accused of.

Trump critical of US Fed

Investors also await news about the health of the housing market, consumer markets, and industrial production. Despite astronomical losses from many US retailers including Sears, retail sales rose by 0.6% in September, along with purchases triggered by Hurricane Florence.

China

With the trade dispute between Washington and Beijing, investors will be awaiting China’s third-quarter reports nervously. Asian stocks also took a tumble last week and the figures released are expected to indicate a cool-off in growth, down slightly from the second quarter.

US Business

JPMorgan led the way with solid third-quarter earnings, followed up by Wells Fargo, and Citigroup. However, as earnings season kicks off in earnest, 54 US companies on the S&P 500 will announce their third-quarter earnings next week, including Morgan Stanley, American Express, and Johnson & Johnson.

With plenty to look out for in the week ahead, one thing is for certain: Traders and shareholders everywhere will be hoping for a better seven days than the ones coming to a close.

Do you want to be a trader? Do you fancy learning how to trade in stocks or bond? If yes, then you have a lot to learn. But first, you’ll need to get acquainted with the terminologies of the trading world.

Trading requires consistent buying and selling of stock, commodities, currency pairs, etc., This is with the aim of accruing or generating profits. Also, a trader is responsible for connecting buyers and sellers so that assets can be exchanged. This is where the trader gets paid for playing the middleman role.

Want to Be a Trader? You’ll Need to Know This

Trading Terms

While you may aspire to be successful as a trader, it’s also important you get acquainted with the world of investing. Gain a clear understanding of a huge number of trading terms. Just like every other industry or field, trading also has its own lexicon.

From beginners to experienced traders, knowing these words is one the salient rules if you want to be a trader. Having a full vocab in trading can keep you grounded in the industry, and give a sense of knowing what it is you are doing.

Here are some of the words to keep in mind so that when you come across them, they won’t seem like jargon.

Acquisition

Acquisition occurs when the shares of a company are purchased by another company, be it in part or in full, for the purpose of controlling the target company. An acquisition is said to take place when a company acquires more than 50% ownership in a target company. In order to consolidate the acquisition process, the acquiring company often purchases the stocks and assets of the target company.

When this is done, the acquiring company has the power to make and take decisions on the newly acquired assets without seeking approval from the shareholders of the target company. A good example is the acquisition of AT&T by Comcast.

There is a number of reasons why companies perform an acquisition. These range from achieving economies of scale, increased synergy, to ramping up market share, new niche offerings, or cost reductions.

Companies seeking expansion to other countries may also consider it imperative to purchase an existing company operating in their country of interest. It’s a viable way of gaining access into a foreign market.

The purchased enterprise is already an established entity with its own personnel, brand name, and other intangible assets which gives the acquiring company a strong foothold to kick-start operation.

Arbitrage

Arbitrage is the simultaneous purchase and sale of an asset in order to cash in on the difference in price. It is a trade that thrives on exploiting the price differences of identical or similar financial instruments on different market platforms or in different forms.

Arbitrage thrives as a result of market inefficiencies. A situation where all markets were perfectly efficient would erase the occurrence of arbitrage. It’s considered a risk-free profit for the trader since the security purchased is sold at a higher price.

It also provides a mechanism that ensures the deviation of prices from the fair value is relatively minimal for long time frames.

Bear Market and Bull Market

A bear market is one in which the sector is rising or is expected to rise. While it’s difficult to predict when exactly a bull market will occur, it is often a result of investor confidence in an asset or market.

This is because “bulls” are currently in control and are making aggressive moves in the market. Conversely, if the market is on a downward trend, it is called a “bear market” because prices are dipping and investors are selling off their shares.

Bear market

CPI

CPI is an acronym for Consumer Price Index. It’s an average of several consumer goods and services that are used to indicate inflation. Movements in CPI are usually projected in percentages–positive movements will indicate inflation, while a movement that negates positive movement means deflation. Central banks make CPI announcements on a regular basis. If you want to be a trader, you’ll need to stay on top of CPI.

ECB

This refers to the European Central Bank, the central bank for the eurozone. The ECB is responsible for setting monetary policies which are highly relevant to traders, as ECB has a significant impact on the value of the euro and European companies.

Also, the ECB’s remit extends to countries that use euro as their currency.

Fibonacci Retracement

A Fibonacci Retracement is an essential technical analysis tool, used to gather insight into when to place and close trades or place stops and limits. Fibonacci retracements mostly depend on the mathematical principle of the golden ratio.

Drawing of six lines across an asset’s price chart: one at its highest point (known as 100%), one at its lowest point (0%), one at its midpoint (50%), and then three at 61.8%, 38.2%, and 23.6% are used to calculate Fibonacci retracement levels.

Gamma

Derived from Delta—which is responsible for measuring the impact of a change in the price of an underlying asset— it is seen as the movement of a delta regarding the cost of the underlying asset.

Hawks and Doves

These terms are used by analysts and traders to categorize members of Central Bank committees by their probable voting direction ahead of monetary policy meetings. Hawks are members who vote for rigid monetary policy at the expense of economic growth.

This translates to a higher interest which could discourage borrowing and encourage saving. Doves, on the other hand, are members who vote for a more flexible monetary policy that keeps interest rates low. This is, in turn, can boost economic growth, increase spending, and increase employment.

This is just a brief introduction to the words you’ll need to know if you want to be a trader. We hope you’ll find these definitions useful and don’t forget to keep yourself abreast of more trading terminologies to make you understand how the trading system works.

It’s been a pretty grim week for global stock markets, although investors can take some solace as Asian markets show signs of recovery this Friday. Large selloffs in US stocks spurred by fears over rising interest rates this week spread to Europe and Asia.

Wall Street saw another sharp fall on Thursday, leading to a losing streak of five sessions for which President Trump blamed the “crazy” and “out of control” Federal Reserve.

Yesterday, the S&P 500 index fell by a further 2.1%, meaning the US benchmark was down by 5% over the week.

When America sneezes the rest of the world catches a cold, and the global FTSE All-World index also retreated for its sixth successive day, erasing all gains made in 2018 and making it one of the worst weeks of the year for global stock markets.

Signs of Recovery in Asia

On Friday, the selloffs continued, but at a slower pace. In Tokyo, shares were down by 0.5% by midday compared to 3.5% on Thursday. Hong Kong shares began the day trading up by 0.4% and shares in Taiwan also rallied by 0.7%.

Futures trading markets also show signs of bouncing back and indicate a stronger opening today for London and New York equities. It seems that after the sharp downturn, global stock markets are beginning to correct themselves with shock charts turning green again in Aisa.

The large selloffs appear to have been triggered by a turbulent US Treasury market and the Federal Reserve’s decision to hike interest rates again. President Trump has been highly critical of the Fed, strongly disagreeing with their decision, and calling the rising interest rates “out of control.”

Global Stock Markets Look to Rally

Global stock markets have been left bruised and battered with the pinch particularly felt in Asia in the wake of the trade war between China and the US. Moreover, account deficit countries such as India and Indonesia have suffered even more as large importers of oil.

We’ll have to wait and see if Asian trading today leads to a firmer start for Europe and Wall Street. But the signs are showing that the global rout in stock is beginning to abate.